Oh hey, remember the times when I posted my annual spending report? Because I skipped it for 2024 (I just forgot all about it at the beginning of 2025), but this time I received a reminder because all the cool kids have been sharing their 2025 spending reports, and because I appreciate those posts, I pulled up our annual report in YNAB* — You Need A Budget – and exported my 2025 data. So you get another post of pretty money pies to look at.

YNAB spits out pretty awesome statistics and reports, but the pie chart was done in Excel (because I excluded certain categories from this spending report, and Excel is just a little better at manipulating and visualizing numbers).

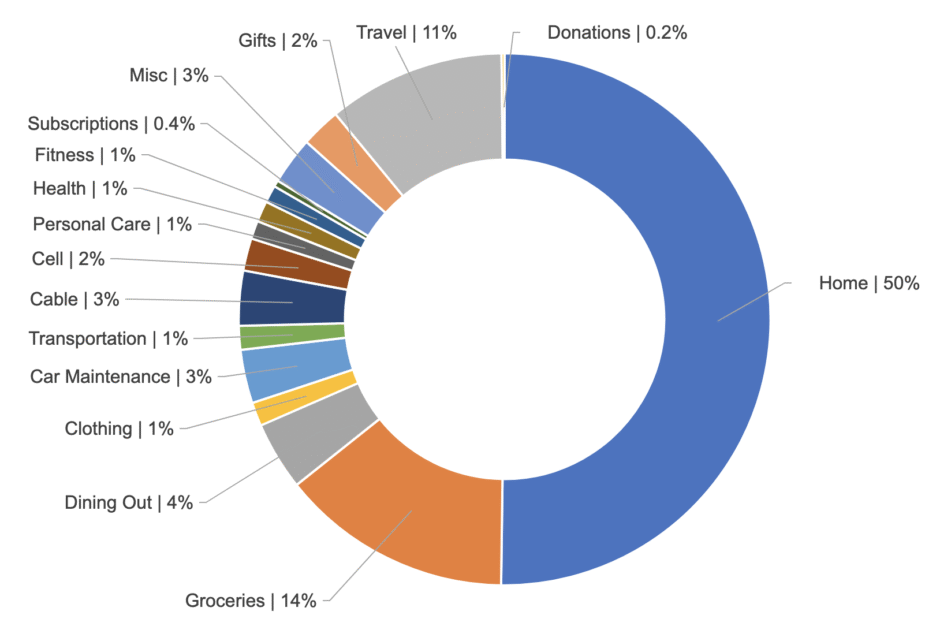

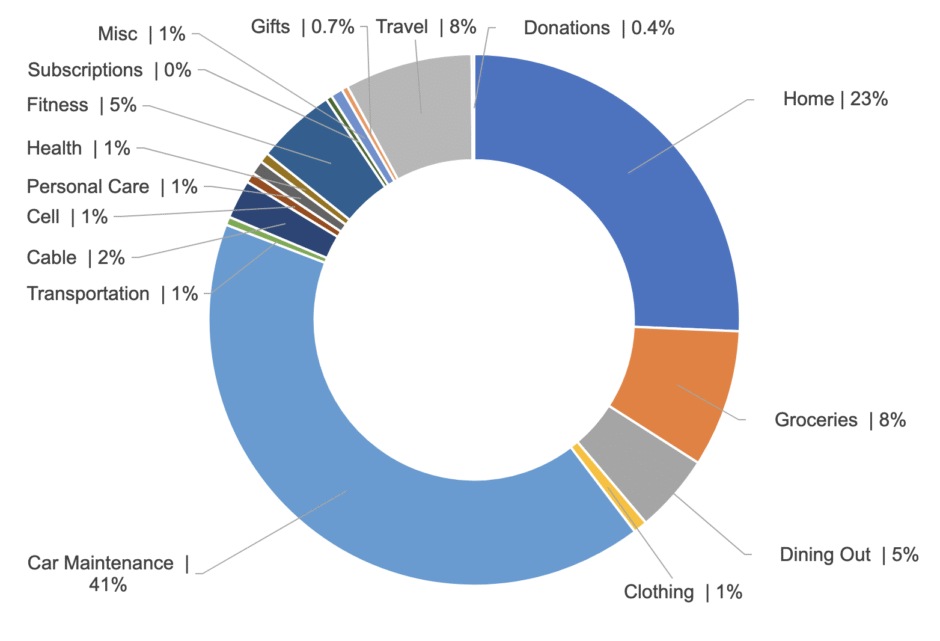

Since I skipped my spending report for 2024 but have the data, I thought I’d share some quick thoughts on our spending. 2024 was a “spendy” year because not only did we decide to move into a bigger, and therefore more expensive rental house, but we also invested in a new car (and yes, we paid cash for it). This is what the money pie looks like when I include the car purchase. Eek.

I feel like it totally skews our regular ongoing expenses, so I created another money pie and excluded the car payment to make the actual expense percentages more comparable. Ah, that’s better.

As you can easily see, a lot of spending categories stayed about the same. There were some fluctuations in actual dollar amounts, but overall spending for most categories was pretty stable. The three categories with the biggest change in percentage of spending were home, fitness, and dining out.

As a reminder: These are percentages based on money spent, not based on my (take-home) income. Not included are savings, retirement contributions, healthcare premiums, taxes, and everything else that is pre-deducted from my paycheck.

Home (50 % was 43 % in 2024)

We moved to a new home (with an office!) at the end of 2024, and our rent increased quite a bit. Home expenses are insane, especially here in California. And as you can see, a good chunk of money goes toward our living situation, but it’s important to me to have a safe and comfortable home and we’re very happy where we live now. It is what it is. The spending for our new (rental) home includes rent, utilities, household items, and rental insurance. It also included other items for our home, like a new couch set and a rug for our living room. The percentage for home expenses was up, and so was the actual dollar amount. Overall spending: ↑

Groceries (14% was 14% in 2024) and Dining Out (4% was 5% in 2024)

We had an increase in grocery spending (what with the inflation going on), but the spending percentage stayed the same. However, we reduced our dining out category quite a bit by about 30% (reflected in a smaller percentage overall), which overall reduced our food category. Overall spending: ↓

Fitness (1% was 8% in 2024)

I continued to pay for my Peloton membership, and I signed up for a couple of (fun) races. The biggest reduction in spending was because Jon stopped working with a personal trainer and quit his gym membership (because we now have access to a small HOA gym that we both use). Overall spending: ↓

Car Maintenance (3% was 41% / 3% in 2024)

As explained in the quick 2024 side-by-side money pies, we pulled out a chunk of cash from savings to pay for a new car. Expenses in this category are for car insurance (which is the biggest chunk), registration, AAA membership, and miscellaneous car maintenance (like oil changes, car wash, etc.). Routine expenses increased slightly due to higher insurance and registration fees. Overall spending: ↑

Transportation (1% was 1% in 2024)

We spent a little bit more on gas in 2025, but I am still thankful for a short commute. The spending percentage stayed the same. Overall spending: →

Cable/Internet (3% was 4% in 2024)

This category stayed pretty much the same in 2025, although I was able to renegotiate our contract, which saved us a few dollars. Overall spending: →

Cellphone (2% was 1% in 2024)

Expenses were about the same. There was a slight increase in spending last year, because we switched to Mint Mobile (from Verizon) and paid a year in advance. Overall spending: ↑

Shopping (3% was 1% in 2024)

We usually spend very little on just random shopping. My biggest purchases were my Apple iPad, and we had some extra expenses for my mother-in-law’s funeral. Overall spending: ↑

Health (1% was 1% in 2024)

We were overall healthy last year, and only had prescription expenses (for Jon) and a few copays at the doctor’s office. Overall spending: →

Gifts (2% was 1% in 2024)

We spent a little more on gifts in 2025. This includes birthdays, Christmas, and ‘just because’ gifts. Overall spending: ↑

Subscriptions (<1% was 1% in 2024)

This includes YNAB, Netflix, blog fees, and our Costco Membership. We cut Amazon Prime last year. Overall spending: ↓

Personal Care (1% was 1% in 2024)

This category includes all toiletry items, make-up, J’s beard trims, and haircuts. Our spending went down a little bit, but the percentage stayed the same. Overall spending: ↓

Travel (11% was 13% in 2024)

We spent a lot of time traveling back and forth to SoCal at the beginning of last year when Jon’s mom was ill. I only paid for one trip to Germany in the summer. Overall spending was down from 2024 (we paid for three trips to Germany that year). Overall spending: ↓

Clothing (1% was 1% in 2024)

We do not spend much on clothing and spent about the same in both years . Overall spending: →

Donations (< 1% was <1% in 2024)

We continue to donate, although it doesn’t really reflect in our spending pie. Work in progress. Overall spending: →

Overall our regular spending was up by 8.3% in 2025. As in previous years, the largest chunk of our money still goes to our home (not surprising in CA) and food. We also continued to prioritize retirement savings/investments as part of our budget (which is not reflected here).

Did you see changes in your spending in 2025? Is housing and important (and huge) expense for you?

* This is not a sponsored post. I have not been compensated by YNAB for mentioning their product.

Lisa's Yarns

January 20, 2026 at 7:51 amHow have you liked Mint? I just bought a new phone so I won’t be able to switch carriers until that is paid for (I gradually pay for it over a couple of years, I think).

As you know, we have no home wedge in our spending pie since we opted to pay off our mortgage several years ago. We are incredibly lucky to be able to do this, but we pay for it by having volatile/intense jobs that infringe on our personal time very easily (both of us routinely work on the weekend). But it is very good feeling to not have a mortgage payment. We still have insurance and taxes but I exclude taxes from our money pie.

Our spending was pretty stable year-over-year. It was not the most precise money pie since Monarch has been a total pain in the you know what. We switched over to Empower but I need to get Phil to add his accounts to it now.

Elisabeth

January 21, 2026 at 7:34 amI love all things spending in blog recaps!!! Thanks for sharing.

I know travel will be a bigger category for us in 2026 because of our Europe trip, but I’m hoping we won’t have any big surprises in terms of home repairs, etc. I feel like each year there is a single “big” expense and we didn’t have that in 2025 (which was lovely), so I feel like we’re overdue for something major to go wrong. (There’s the pessimist in me shining through!)

Meike

January 21, 2026 at 9:34 amHousing is a pretty big expense for us, too – living where we do I guess that is not very surprising and I bet last year work on the house would have been a big chunk as well considering we did update our electrical. Nothing much changes otherwise. I usually take a closer look whenever I know I have a big expense coming up. Next thing will be college for the kids.

ernie

January 21, 2026 at 1:09 pmI hate how much your housing costs. Eek. That’s rough. I do not track my finances. Who even am I? I’ll tell you what – I grew up the daughter of an accountant who worked as a controller . . . and he was, still is, controlling. We are careful with our money in general, so I don’t hover over the numbers. I probably should.

K @ TS

January 21, 2026 at 3:35 pmI had that same issue when I bought my car; it really made my pie lopsided! I actually put it in that year, but when I did my averages over the years I kind of prorated it (with an estimated life) so I could get a more accurate estimate of what my annual transportation costs would be.

Stephany

January 21, 2026 at 6:05 pmThat’s amazing that your spending has stayed so steady over the past few years, especially with inflation and CoL! Housing/bills are definitely my biggest expense, and second to that would be food.

Tobia | craftaliciousme

January 24, 2026 at 3:49 amAll these money pies tell me I need to sit down and do some work on my financials. I have no idea how my spendings are. In 2025 I was constantly eating away at my saving since my wage didn’t cover expenses. So this year I gave myself a raise and for now it works but not because I know what’s going on. So yeah… I am flying blind.

We have cut streaming services in 2025 though and I haven’t missed it.

Sara

January 24, 2026 at 6:50 amIt’s so interesting to see what expenses remained relatively flat for you! Housing is the biggest part of our budget, and it continues to go up even though we’re paying down our mortgage in advance and have a VERY GOOD interest rate (bought in 2014). Property taxes in Texas are very high, and we live in an area that continues to rise in value and the tax authorities don’t really negotiate regardless of protesting the value. (I will say that it’s a bit of a moral hazard as well… our property taxes fund public education, so fighting our property taxes makes me feel like I’m part of the problem… so generally, I’ll pay my property tax (with just a little grumbling). Our car maintenance costs are also very steady. I realized last week that this is the first time we’ve taken our car in for break work. (We have a 2010 Toyota that we paid cash for… in 2010.) It was $600, and when I think about that over the 16 years of the car, I think it’s pretty good ROI. ;) My car, which is a 2008 Toyota (my big purchase after college that I also paid cash for!), needs some work, but I now that we’ve found fair and reasonable mechanic, I think we will spend the money to get her running again this year. So, after several years of declining auto expenses, we might have an increase this year. I think what’s most interesting is that we did find out that we *could* be a single car household, which I think is pretty rare in Dallas. It also means that if the mechanic can’t bring my car back to life, the only sadness that I’ll really have is letting go of the nostalgia that comes with having bought that car on my own (and the great day that my stepdad and I had negotiating for it), and not that I need to buy a new car. ;)