I am jumping on the bandwagon. I previously shared my ‘end of year’ spending report with you, but it probably is more insightful to give updates along the way. Because if one thing that I mentioned in my budgeting review is true, is that your spending will shift throughout the year. I’ll explain what I mean in a second.

I wish I could be a bit more transparent about actual dollar amounts because I think that would be really, really helpful, but I haven’t worked up the courage (yet). Also, there are so many floating pieces that people include or exclude in their budget and so it’s really hard to get a complete picture.

I personally think you should always budget with your net pay, although that can vary tremendously depending on what your pre-tax deductions are, and in my case, that means a huge chunk of money has already gone away to taxes, healthcare, and retirement fund before I even see it. My take home is 59% of my gross pay. That makes a big difference, doesn’t it? I mean, I would love to have a bigger chunk of my money to take home, but I am also trying to maximize my contributions. What’s the percentage of your take-home pay? Do you prioritize deductions for life insurance, healthcare, and retirement?

When finance articles say that you shouldn’t spend more than 30% of your income on housing. Does that mean 30% of your gross or net pay?

Also, does 30% mean “just for rent” or does it include all the other expenses that come with housing (like utilities, renter’s insurance and/or taxes, home improvements, etc.)? Most finance articles are not very clear on that. However, what is pretty clear is that 30% for someone on a lower income is a lot harder to handle for someone on a higher income.

We should discuss these aspects a little more, but maybe we save this for another post. Back to the quarterly spending summary.

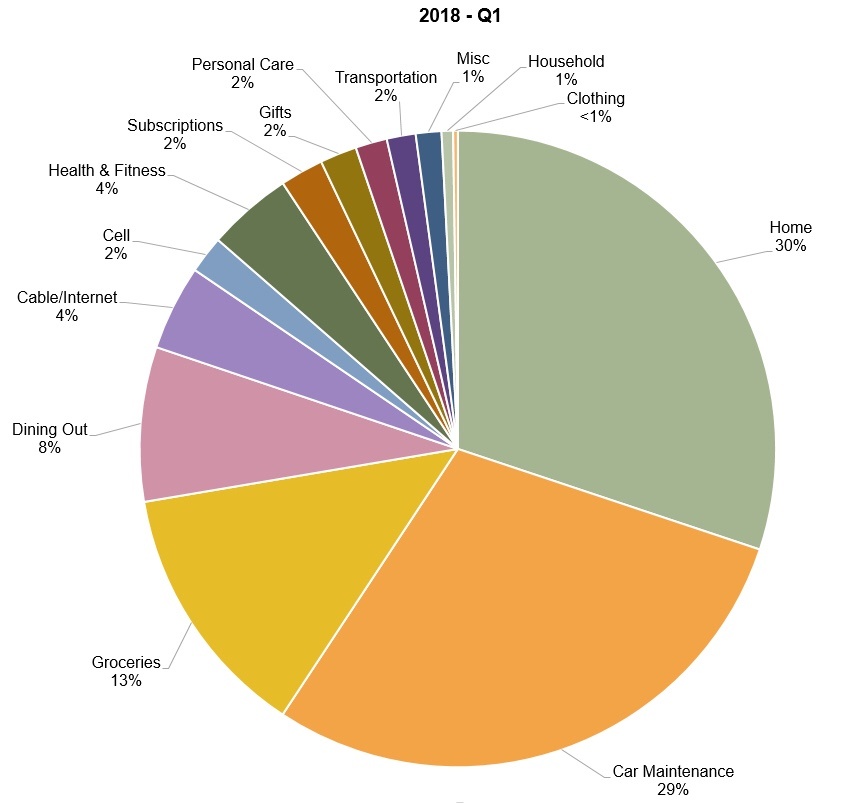

As you can easily see from this handy pie-chart (which I pulled out of YNAB), more than half of our spending in quarter 1 of 2018 went to our home and car maintenance. Ouch. That hurts a little. I have more subcategories that I track separately in my budgeting software, but I consolidated them a bit for the purpose of easier visualization. As a reminder: these are percentages based on money spent, not based on my (take-home) income.

Home (30%) – The spending for our home includes mortgage/taxes, utilities, and maintenance cost. We also had a minor repair earlier this year.

Car Maintenance (29%) – We had an unexpected car repair, we had to buy new tires and our 6-months car insurance and registration was due – all in the first three months of 2018. Fun! This is why it is so important to budget for these kinds of things throughout the year because they can otherwise throw off your whole budget in a three months period.

Groceries (13%) and Dining Out (8%) – While I have brought down our grocery spending quite a bit, we still spend a larger percentage on groceries than other people (from what I can tell). As you can see, it’s also separate from our ‘dining out’ category. I will say that we ate out a bit more than usual in the last few months and I am hoping to reign this in a bit in the second quarter.

Cable/Internet (4%) – Yes, we still pay for Cable and Internet is not cheap.

Cellphone (2%) – Self-explanatory.

Health & Fitness (4%) – This category includes my gym membership, my Runtastic subscription, and our medical and dental co-payments. I didn’t include our health care premiums this time because they come out of my paycheck pre-tax, but wondering if I should?

Subscriptions (2%) – This includes Netflix and a few annual subscriptions that are due at the beginning of the year, like Amazon Prime and MLB TV.

Gifts (2%) – Birthdays, mainly.

Personal Care (2%) – This category includes all toiletry items, makeup, and haircuts.

Transportation (2%) – Gas and parking fees. Everything else car-related went into the car maintenance category.

Misc (1%) – All the spending that doesn’t really fit into other categories, e.g. our identity guard monthly fee and other purchases.

Household (1%) – Household items. Everything from toilet paper to laundry detergent to cleaning items.

Clothing (<1%) – Did not spend much on clothing at all. It barely made this list.

Travel (0%) – No expenses for travel in Q1 of 2018. Sad face. I mean, I did spend money on my flight home (that I had to cancel), but I still have the voucher for the flight, so I’ll count this when I use it.

Where did most of your spending go in the first quarter? Did you have any unexpected expenses?

Ana

May 7, 2018 at 9:02 amThis is really interesting! I know I need to put more towards my retirement, but right now I’m not in a place to do that.

how do you get such a detail percentage or toiletries and household? Do you input all your purchases somewhere? I count those as groceries.

My unexpected expense this year, was having to pay for a passport. A necessary expense, but still unexpected.

san

May 8, 2018 at 11:52 amI am using YNAB (link in post) to budget and track our spending. It’s been really eye-opening but it has also made me think A LOT about finances.

suki

May 7, 2018 at 11:26 amFrom what I’ve gathered, it’s 30% of gross. You already know where I’m at with my Q1 spending. Another question of mine was whether to include the rental property or not. It’s a work in progress, so my Q2 report might be formatted a little differently.

san

May 8, 2018 at 11:53 amI read too that it’s 30% of gross, but it seems like it should be from your take home pay.

If you have a rental property that provides income, I would include it… of course, you also have expenses associated with that, I assume.

Beth

May 7, 2018 at 2:17 pmWe’re using a similar format to this for tracking our budget as well. We found we were spending FAR too much on food, so we’ve been trying to cut back on that without denying ourselves meals obviously, but have been trying to cut back on the things that we don’t truly need and have been trying to eat out less.

san

May 8, 2018 at 11:54 amI don’t know how bring down our food budget any more… LOL we enjoy food and I already mealplan and shop sales (and we don’t throw any food out). We could eat out less, I guess.

Charlotte

May 7, 2018 at 2:49 pmI love pie charts, because I’m a pretty visual person and it helps to see the breakdown in this way. I never know if you’re supposed to figure out pre- or post-tax earnings either, but to me it makes sense to calculate based on your takehome pay at the end of the month. That said, I need to do something like this. I feel like way too much of our money goes to food/dining out. I’m trying to cut back, too, but sometimes I get lazy and don’t go food shopping and (insert excuse here). Ha!

Thanks for sharing this!!

san

May 8, 2018 at 11:55 amI LOOOOVE pie charts. I am a very visual person too and it just helps to see it broken down like this : )

How much do you spend on groceries if you mind me asking?

Charlotte

May 15, 2018 at 7:49 amWe typically spend between 300-400 a month on groceries. We also go out at least once or twice a week and spend money on food, which I’m hoping to reign in a bit more. Yesterday I made a big batch of vegetable korma and I realized I’m not such a terrible cook when I put the time in!

ShootingStarsMag

May 7, 2018 at 5:54 pmI find this fascinating, even if you don’t share actual numbers. I can understand how that would be a bit awkward to do! Sorry you had to spend so much on car maintenance, but hopefully that will be better next quarter.

-Lauren

san

May 8, 2018 at 11:55 amI agree, it already is interesting without actual numbers, but sometime I feel it would be even more transparent to talk about what people actually budget with.

Akaleistar

May 7, 2018 at 6:17 pmI’m tracking my expenses in my planner, and it’s so interesting to look back and see what I’ve been spending money on. Saving up for unexpected expenses is really important.

san

May 8, 2018 at 11:56 amDo you just track for fun or do you use it to make adjustments in your budget?

Akaleistar

May 8, 2018 at 6:38 pmIn theory, it’s so I can stick to my budget and see where I am overspending. I don’t always stick exactly to my budget, but writing my expenses down helps me to be more conscious about spending money. Plus, I like finding reasons to use my planner :)

anthea

May 8, 2018 at 5:07 amI agree with Charlotte – I like the pie chart and it sets everything out so clearly.

Sorry about your car repairs – never fun but often costly :(

san

May 8, 2018 at 11:56 amI LOOOVE pie charts :)

Stephany

May 10, 2018 at 12:26 pmI love this! I don’t mind sharing actual numbers because it’s just lil ole me here, so I’m not accounting for someone else’s spending. It would be different if I had a partner!

Car repairs are the worst! I had an expensive one in Q2 and I’m hoping I don’t have any other ones to deal with. They are so not fun!

uit

May 14, 2018 at 9:24 amIt’s so smart to do this quarterly so you can make changes if you notice spending that is creeping up! I only do a spending post annually but I do look at it throughout each month so I can see where our money is going. These days I am not spending much money since I’m home with Paul so discretionary spending just isn’t really happening – besides buying baby stuff we need which I don’t realy think of as discretionary (I think of discretionary as things like eating out, entertainment like movie tickets, travel, clothing, etc).

So from my time in the mortgage industry, I learned that all of those housing ratios are based on gross income. So when articles say you should spend 30% of your income on your home, I think they probably mean gross income. But it’s hard to say for certain. Our housing payment is really low as a percentage of our income because our house is really small and we bought it before the more recent surge in home prices. We are home shopping now but won’t purchase something that is 30% of our income because we want to be conservative about our house payment in case one of us ever lost our job. Phil and I both work in a really volatile industry and it’s the same industry (financial services) so our income isn’t diversified. So we are very risk-averse when it comes to buying a home.

Car repairs suck. I hate spending money on cars. Luckily Phil and I both have new’ish cars that don’t have many miles on them so *hopefully* we won’t have car repair expenses for a long time. But 2 years ago my car died on the way back from my parents’ lake home so I had to unexpectedly buy a car. That sucked so much! But I barely drive so that car doesn’t even have 10k miles on it now so I’m hoping it lasts for many man y years!!

terra

May 23, 2018 at 5:12 pmI’ve always wondered about the 30% for living expenses and what *exactly* that means. I spend about 28% on my mortgage, but then there’s additional expenses for my household bills. I just checked Mint and it looks like my mortgage is the thing I spend the most on, followed by travel, which I’m totally ok with. It’s definitely neat to break it all down by percentages and see where the money goes by category.