© ynab.com

As I mentioned in my Spending Report post earlier this year, I wanted to give you an updated review of the budgeting software I’ve been using for the last 3 years. I reviewed You Need A Budget (referred to shortly as YNAB*) once before, but that was before they migrated their software to an online subscription service a couple of years ago.

To be honest, at first, I wasn’t thrilled to be forced to go from a one-time desktop purchase to a subscription-based service (although that seems to be the direction many software are going these days), but I quickly made my peace with it because a) I just really like the software and b) the annual fee is totally acceptable and worth it to me. (To be completely transparent, I have to disclose that since I was a previous YNAB user, my subscription was grandfathered in after the migration and my annual subscription fee is lower than what they advertise on their website now. I still think it is worth the cost.)

The basic budgeting approach hasn’t changed. What sets YNAB apart from other money tracking software is that with YNAB you’re not just tracking your spending (in retrospect), but you’re looking ahead and assigning dollars for future expenses. Think of it as your income divvied up into little pots that hold the money for each of your monthly expenses, emergency fund, and long-term goals, and you always know exactly how much is in each pot.

Initially, I found it helpful to divide our spending into three categories:

- fixed expenses (e.g. rent, Internet, subscriptions, etc.) that are the same amount every month,

- fixed expenses with actual numbers that might slightly vary (e.g. gas, electric, groceries, etc.),

- irregular recurring expenses (e.g. car insurance) that only have to be paid once or twice a year, but you still need to budget.

Once you have a ballpark number for those expenses and know how much you have left over to put into an emergency fund, savings, and discretionary spending, you can start building a budget.

YNAB’s budgeting approach still works with four simple rules. They have been rephrased since the early days, but the idea is basically the same.

Rule One: Give Every Dollar A Job

Rule One: Give Every Dollar A Job

Rule One: Give Every Dollar A Job

Rule One: Give Every Dollar A JobThe secret is to be intentional about what you want your money to do before you spend it. Look only at the money you have on hand and ask yourself, “What should this money do before I’m paid again?” You either budget it towards your expenses or decide to put it into savings, but nothing is left “unbudgeted”. If you have all your fixed expenses budgeted, the leftover money can help to “cushion” your expense categories to ‘have a little extra’ just in case, go into your emergency fund, or towards “fun money”, but regardless of where it goes, you have to assign it a ‘job’.

What I do:

At the beginning of each month, I put money for all fixed expense (mortgage/rent, utilities, other bills) in the appropriate category. I also always budget a certain amount towards groceries, fun money, gifts, etc., even though I know that those are numbers that will fluctuate every month (but at least, I have a ballpark number in my budget. This is where rule three comes in!).

Rule Two: Embrace Your True Expenses

Rule Two: Embrace Your True Expenses

Rule Two: Embrace Your True Expenses

Rule Two: Embrace Your True Expenses(used to be “Save for a rainy day”)

This second rule helps you budget in advance for less-frequent, but recurring expenses (like the car registration, quarterly insurance premiums, Christmas, etc.) and also helps to stash away some funds for expected, but less predictable expenses (like car repairs, vet bills, etc.) By putting a little bit of money in these categories every month, you embrace your true expenses by setting money aside for them in advance. You’ll have peace of mind that you’ll have the money in your account when the bill comes due. No “shit-I-forgot-about-this-bill”-surprises anymore!

What I do:

I divvy up irregular, reoccurring bills (like insurance payments, annual subscriptions, etc.) into “monthly payments” and budget that amount in the appropriate category every month. That way I make sure that I have the money sitting in my account when the bills come due. I also budget a small monthly amount in categories that could trigger an unexpected expense (e.g. car maintenance, home repairs.)

Rule Three: Roll With The Punches

Rule Three: Roll With The Punches

Rule Three: Roll With The Punches

Rule Three: Roll With The PunchesA budget is not rigid. It not only will, but needs to be adjusted every month. The goal of budgeting is not to be able to anticipate your spending down to the penny and stick to the same budget amounts every month. It’s simply not feasible. Life is not predictable like that and every month will be a little bit different.

The goal is to ‘roll with the punches’ and adjust and tweak your budget every month accordingly. Overspent in one category? Make adjustments (e.g. take away some dollars from another category to cover the extra-costs). If you can’t or choose not to, the software will automatically deduct the overspent amount from next month’s money and you’ll just have to tighten your budget next month. On the flipside: if you don’t use the budgeted amount in a category, it will roll over to next month, too and you’ll have a little extra money as a buffer. Not every month will be the same, but you can strive to balance out between the months. It all comes down to try really hard to just spend what you have!

What I do:

I absolutely embrace this rule.

I think this rule is one of the most important rules to keep in mind because people forget (or falsely believe) that if they set a budget, they must live by it ‘down to the dollar’ and that is not just exhausting to think about, but also highly unrealistic. No wonder people have bad connotations of the word ‘budget’.

If we have leftover money in the grocery category, for example, but ate out more than usual, I ‘transfer’ money from the grocery category to the ‘dining out’ category for that month to the cover the shift in expenses. I also sometimes simply roll over leftover grocery money to the next month because I know that during a month where I do a Costo-run, my grocery budget will automatically inflate a little bit.

Rule Four: Age Your Money

Rule Four: Age Your Money

Rule Four: Age Your Money

Rule Four: Age Your Money(used to be “Live on last month’s income”)

You want to increase the time between the moment you earn a dollar and the moment you need to spend it. The longer each dollar sits in your bank account, the ‘older’ it will be. The concept follows a ‘ first in, first out approach’, so the dollar you made in the previous month will be spent before the last dollar that you made.

This last rule is really geared towards people who currently live paycheck to paycheck and struggle every single month to pay their bills because they’ll be covering those bills with money that don’t yet have in their possession. The goal here is to save up enough money (roughly the equivalent to what your regular monthly income is) and then live off that money the following month. This is not technically ‘saving’, it just means you’re creating a buffer in your bank account, so you’ll always be “one month ahead”. So, to get to the ‘last month’s income” point, your money needs to be at least a month (30 days) old. Of course, the more you age your money, the more financially secure you will feel.

What I do:

We’re luckily in the position now that we already budget for the current month with last month’s income. So, even though I don’t have any debt to pay off and savings that I can dip into if need be, this way of thinking about your budget and how to manage your money makes a lot of sense to me. I treat every month as if I only had last month’s income available. I know that fixed amount (I get paid bi-weekly, so it’s usually two paychecks) and can budget with that amount for the month.

The interface

This is what the (new and improved) interface of the software looks like (obviously, this is just a test screenshot, not my budget).

It’s completely customizable. You can create new categories, organize them in different ways (by pay cycle, importance, alphabetically…) and delete categories you don’t need. In the left column, you add your accounts (I listed all my bank accounts, credit card accounts, store card accounts, Paypal, and yes, a cash account).

The software pulls in online account information automatically, only cash expenses have to be filled in manually. You can split transactions into multiple categories (which I routinely do after, let’s say, a Target run, where I bought groceries, personal care items, and household goods) which makes tracking your expenses by category really easy.

So, at the beginning of each month, you budget all your recently earned money (which will show in the green box at the top) into the different categories in the “budgeted” column, the software keeps track of your spending in the “activity” column and the “available” column tells you how much money is then available for each category. Ideally, the green box shows “zero”, when you have budgeted all your money.

Once it’s all set up, working with your budget is really not all that time-consuming. I sit down once a week after my weekly grocery run and check in with my budget. That usually doesn’t take more than 30 minutes (often less). When I spend cash, I immediately put the cash expense into the app, so there is no discrepancy when I review my budget online. And then, I reconcile my account at the end of each month to make sure I didn’t miss anything and all numbers add up. I find this interactive part highly valuable in the budgeting process because you’re forced to log and look at every individual expense.

Why I have stuck with this budgeting software.

1. The software has an easy to use, eye-pleasing interface and to me, it feels pretty intuitive. I love that you can customize every part of it to your needs (you can add categories and omit the ones that don’t apply to you.)

2. I love that the software goes hand in hand with a very handy app that makes tracking “on the go” really easy and then automatically syncs with the web version.

3. YNAB has been an invaluable tool to keep on top of all our irregular, recurring expenses throughout the year. I know where our money goes at any given moment. I have gained a better understanding of our spending habits and priorities.

4. One of the most important parts of this budgeting approach for me is that I don’t pay much attention to my bank account balance anymore but instead look at the ‘available column’ in the software. My bank account shows me all the money I have, but because this money is set aside to cover various upcoming expenses, the ‘available column’ has much more meaning. You put in your spending as you go and the software does the math for you and always tells you how much more money is available for each category for the rest of the month. By just looking at how much is available in each spending category I make sure that I know how much I can spend while meeting all my other financial obligations.

Conveniently, you can check this in the app while you’re out and about and before making any purchases. Talk about holding yourself accountable!

5. Since it’s now a web-based service, I can access it from anywhere. I initially thought that wouldn’t be something that wasn’t important to me, but I realized: it is. It’s convenient to be able to check in with your budget wherever you are.

For me, YNAB just works.

Phew. This post got longer than I thought. Can you tell, I have a lot to say about YNAB. Let me know if you have questions for me. I’d be happy to help.

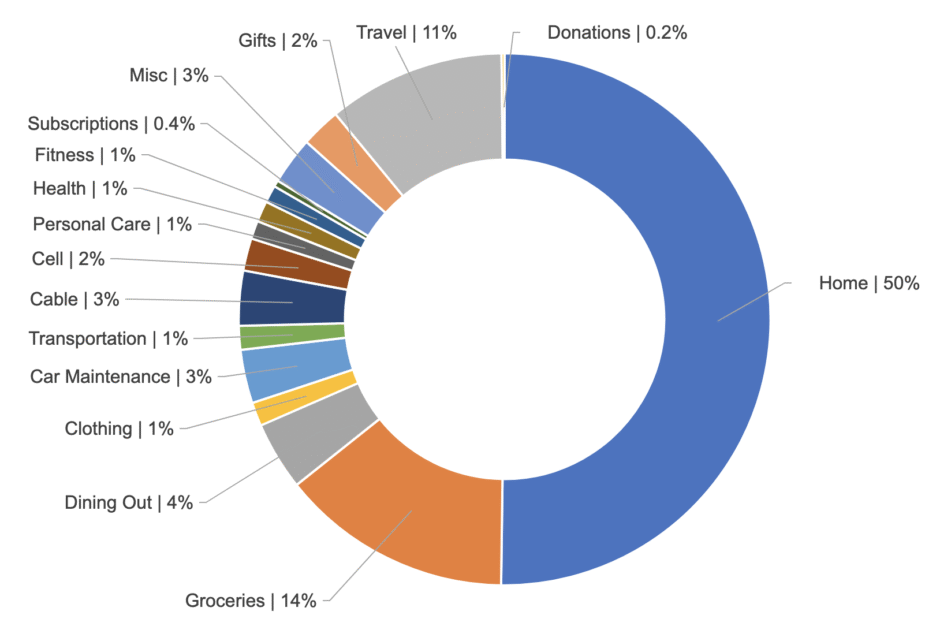

In case you want even more information, YNAB creates insightful reports that will give you pie charts, spreadsheets and more in response to all your pressing questions about your budget. Our ‘spending report‘ post from earlier this year was created with the help of YNAB’s budget reports.

YNAB also has a very informative blog and offers online classes if you need help to get started or if you’re having trouble with a particular issue. Their help team is also very responsive, in my experience.

* This is not a sponsored post. I have not been compensated by YNAB or anyone for this review. The opinion is solely my own. However, the post does contain affiliate links. If you feel like this software could be for you, download the fully functioning trial version and give it a shot! If you like it, you can use this link to activate the software and we’ll both get a month free!

Beth

April 17, 2018 at 7:44 amThis is a timely read for me, we’ve been talking about giving YNAB a try. I will share this info with my husband, thanks for all the information!

Akaleistar

April 17, 2018 at 11:15 amThe age your money concept is really interesting!

Meesh

April 17, 2018 at 12:54 pmInteresting! That “$300” on rent/mortgage a month in their demo is really CUTE LOL. Clearly their headquarters are not on the coasts. LOL. I once heard on a podcast that most people don’t have savings enough for a $1000 emergency, should it occur. That made me feel a whole lot more secure than I truly feel every day a single lady on a very middle class budget, paying mortgage/bills etc all on my own. It gave me that “I REALLY AM DOING OKAY” moment.

Lecy | A Simpler Grace

April 17, 2018 at 4:54 pmI’ve been needing a good budgeting software! I love the detail you went into in this review and I think it’s awesome how easy YNAB makes it to track both fixed and flexible expenses.

ShootingStarsMag

April 17, 2018 at 7:16 pmThanks for sharing all of this! I love that it shows the amount of money you have in your categories and not just all the money actually available. That’s one thing I wish a bank account would do.

terra

April 19, 2018 at 5:57 amI’m always fascinated by how people spend and budget their money and I know a lot of people have found great success with YNAB. I’m a big fan of Mint and it’s worked for me so far and I feel like I finally realized my budget needs to be more flexible. I used to get frustrated when things didn’t match what I’d set aside, but I’ve gotten a lot better about being honest about my spending and shifting money around depending on what I’ve got going on in a given month and that’s helped a lot. And saving for those occasional big expenses, like car insurance, month to month instead of just forking it out all at once has been a huge help, too.

Stefanie

April 19, 2018 at 9:08 amI haven’t used a budgeting software in a while but I’ve always been a big fan of Mint rather than YNAB. I still have my Mint account but haven’t logged in in a while. Maybe I should…

…I have been doing okay going from two incomes to just one. Mainly because my salary accounted for 2/3 of the combined income. I did make some adjustments during the transition period (lowering my retirement contributions) but now that I’m somewhat settled and comfortable with my new bills, I think I am going to up them again. There are a lot of things that are much cheaper in NC compared to WA which also helps a lot.

Lisa of LiSa’s yarnS

April 19, 2018 at 3:51 pmI use Mint which is not as great as this but does the job for me. YNAB sounds like a great application, though. I use mint but Phil doesn’t. He figures he spends so little (which is true) that he doesn’t need to watch his spending so closely. But I like to see where my money is going even though I know I am spending the right amount of money. I should be better about breaking out target spending. And i should reclassify amazon purchases!

Stephany

April 19, 2018 at 5:40 pmOh, I love this so much! I continually say that I want to set up YNAB and get better control over my finances, but I think I’m a little overwhelmed by the thought of setting it up. And I feel like I’m so far away from that ideal of “aging your money” that I just don’t even want to try. (I’m great at being an adult, is what I’m saying.)

Maybe I’ll make it a goal for the second half of 2018 – finally start using YNAB!

Kathleen

April 20, 2018 at 11:13 amI might have to give this a try! I use a spreadsheet and Mint, and it works fine. But that “Available” column is verrrry enticing!

suki

April 20, 2018 at 8:35 pmGreat review! I’ve been using it since your recommendation last time! :) Really wish the improvements would keep on rolling in since they’re online now.

san

April 22, 2018 at 8:17 pmThanks! I am glad you like it!